With employers looking for ways to contain costs, maintain benefits, and decrease the burden of regulations, all while helping improve employee health, the self-insurance market has opened up to the mid-sized market with plan options that give employers control without having to assume all the risk.

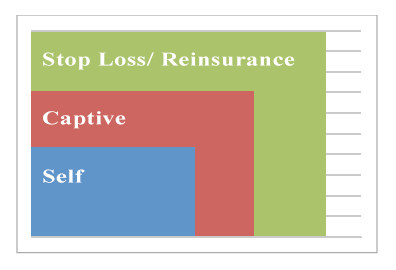

One such option is the level funding plan. Employers use a TPA to access a network, administer the plan, adjudicate claims and negotiate stop loss coverage. Premiums will be based upon maximum cost estimates for the year. If the amount of claims exceeds the funding balance, the stop loss coverage will pay the difference. If, at the end of the plan year, the claims have been lower than the expected maximum, the surplus funds will be used to offset future costs.

A captive works similarly to the partially self-funded model above, but has an additional layer of protection. With this model, the client will pay the initial claims up to a specified amount. Premiums will be based upon expected claims. That level funded premium will include funding the captive, which serves as a buffer between the company and high cost claims. Stop loss coverage will pay claims above the captive threshold. Any balance at the end of the year left in the captive bucket will be split between the clients to offset future costs.

Both models allow employers to customize their plan to best suit their population. Because they are governed by ERISA, these plans are not subject to many state mandates and some reforms and fees of the ACA. They also present a great opportunity to establish a wellness program that has a positive impact: the healthier your employees, the lower your claims costs.

Not all alternative funding solutions will be the right fit for all companies. Your DG advisor can review the risks with you to determine whether self-funding is a viable alternative for your group.